Private credit has scaled into a core allocation across institutional portfolios, exceeding $1.7 trillion in global AUM. The asset class, once defined by structural inefficiencies and lender discipline, is now characterized by capital saturation, competitive deal dynamics, and increasingly asymmetric risk profiles. Observations from large-scale credit managers suggest that the market is no longer in an expansion phase driven by opportunity, but in a late-cycle phase defined by excess capital and weakening underwriting standards.

Structural Foundations and Their Evolution

The growth of private credit was initially underpinned by three durable factors: bank retrenchment following Basel III, prolonged yield suppression during the ZIRP era, and the expansion of sponsor-driven leveraged buyouts. Direct lenders filled the void left by regulated banks, offering speed, flexibility, and floating-rate structures that aligned with investor demand for income.

However, those same forces have matured. Bank participation has partially returned in certain segments, yield is no longer scarce in absolute terms, and private equity activity has normalized. The supply of capital dedicated to private credit now exceeds the availability of high-quality lending opportunities, fundamentally altering the balance of power between lenders and borrowers.

Capital Saturation and Competitive Degradation

The defining feature of the current environment is excess capital competing for a finite set of deals. This has manifested in several ways:

- Spread compression relative to underlying risk

- Increased borrower leverage, often justified through aggressive EBITDA adjustments

- Covenant-lite or covenant-loose structures becoming standard in sponsor-backed transactions

- A shift from bilateral negotiations to broadly syndicated “club” deals among private lenders

These dynamics represent a departure from the original private credit model, which relied on structural protections—particularly covenants and seniority—to mitigate downside risk. As those protections erode, the asset class begins to resemble syndicated leveraged finance, but without the same level of price transparency or liquidity.

Illiquidity and the Illusion of Stability

A central premise of private credit is the illiquidity premium. Investors accept capital lockups in exchange for incremental yield. In practice, however, the current environment raises questions about whether this premium is being appropriately captured.

Reported volatility in private credit remains low, largely because valuations are based on infrequent marks rather than continuous market pricing. This creates a smoothing effect that obscures underlying credit deterioration. At the same time, secondary markets for private loans remain thin, limiting price discovery and exit optionality.

The result is a structural mismatch between perceived and actual risk. Investors may interpret low volatility as evidence of stability, when in reality it reflects delayed recognition of credit stress.

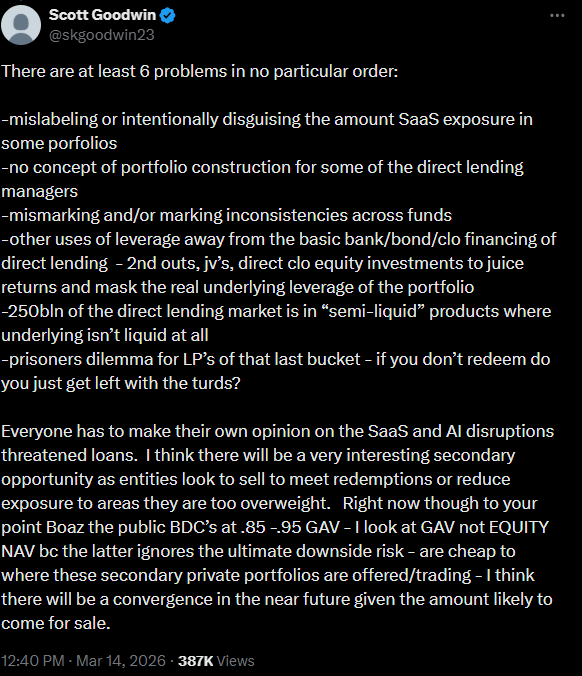

One of the most fascinating credit investors, Scott Goodwin, recently posted about the issues with the private credit market on X:

I really liked his episode on Goldman Sachs Exchanges; he provides some good incites and has a fun story.

Emerging Risk Factors for Private Credit

Several risk vectors are becoming more pronounced as the cycle matures.

First, higher base rates are exerting pressure on borrower fundamentals. Interest coverage ratios are compressing, particularly for highly leveraged issuers that were underwritten in a low-rate environment. While default rates remain contained, amendment activity has increased, suggesting early signs of stress being managed through maturity extensions rather than balance sheet repair.

Second, liquidity mismatches are embedded in many retail-oriented private credit vehicles. Interval funds and non-traded BDCs offer periodic redemptions despite holding illiquid assets. In a stressed scenario, this structure introduces the potential for forced selling, gating mechanisms, or NAV dislocations.

Third, spreads have not widened sufficiently to compensate for incremental risk. In effect, investors are accepting tighter yields for loans with weaker structures and higher leverage. This creates a negative convexity profile in expected returns, where downside risk expands without a corresponding increase in income.

SaaS Lending and the Impact of AI

The most fragile segment within private credit is lending to SaaS and technology-enabled businesses. Over the past decade, these borrowers became a preferred target for direct lenders due to recurring revenue models, high gross margins, and the perceived durability of software-driven business models.

This led to underwriting frameworks that emphasized revenue growth and annual recurring revenue (ARR) rather than traditional cash flow metrics. Leverage levels increased accordingly, often supported by covenant flexibility and optimistic projections of long-term growth.

That framework is now being challenged by advancements in artificial intelligence.

AI is reducing the cost and complexity of building software products, accelerating development timelines and lowering barriers to entry across many SaaS verticals. As a result, competitive intensity is increasing. Pricing power is weakening, customer acquisition costs are rising, and retention dynamics are becoming less predictable.

For lenders, this introduces a fundamental shift in risk. The assumption that SaaS businesses possess durable competitive moats is no longer as reliable. Revenue stability, which underpinned credit underwriting, is now more uncertain.

The implication is that many loans to SaaS borrowers were priced and structured under assumptions that may no longer hold. While near-term performance may appear stable, the distribution of outcomes has shifted. Downside scenarios are more severe, and recovery values in stress cases may be lower than expected.

Market Signals from Professionals in Private Credit

Feedback from experienced credit managers indicates a consistent set of observations:

- Transactions are being executed with looser structures than would have been acceptable earlier in the cycle

- Competition among lenders is driving concessions on both pricing and documentation

- Sponsor behavior is becoming more aggressive, with less equity cushion in certain deals

- Risk is migrating from regulated banking institutions to less regulated private capital pools

These signals do not imply an imminent dislocation, but they do point to a gradual erosion of credit discipline across the market.

Implications for Portfolio Construction

Private credit remains a viable component of a diversified portfolio, but its role should be reassessed in light of current conditions. The asset class no longer offers a straightforward illiquidity premium supported by strong structural protections. Instead, outcomes are increasingly dependent on manager selection and underwriting discipline.

Allocations should prioritize first-lien senior secured exposure, covenant protection, and sectors with stable, non-disruptive cash flow profiles. Managers with demonstrated experience across credit cycles are better positioned to navigate deteriorating conditions.

Conversely, portfolios with high exposure to growth-dependent lending, particularly in SaaS-heavy strategies, carry elevated risk. Covenant-lite structures and vehicles with embedded liquidity mismatches should be evaluated critically.

Going forward with Private Credit

The next phase of the private credit market will likely be defined by its migration from institutional portfolios into more semi-liquid and fully retail-accessible structures. Historically, private credit has been dominated by institutional allocators: pensions, endowments, and sovereign wealth funds, who were able to tolerate long lockups, limited transparency, and valuation subjectivity in exchange for yield premiums over public credit. That dynamic has been shifting and will continue to shift more rapidly.

Asset managers are actively engineering products that bridge the gap between institutional private credit and retail accessibility. This includes interval funds, tender offer funds, private credit exposure in ETFs, and ETF-like structures that package private loans into structures with periodic liquidity.

The objective is clear: expand the investor base and capture a growing pool of retail capital seeking income in a persistently uncertain rate environment. For retail investors, the appeal is straightforward—yields that exceed traditional corporate bonds, often marketed with lower volatility due to infrequent mark-to-market pricing.

However, this structural evolution introduces a critical tension between accessibility and risk transparency.

On one end of the spectrum, there are well-constructed vehicles designed to thoughtfully democratize access. These platforms focus on senior-secured lending, maintain conservative loan-to-value ratios, and implement liquidity management frameworks that align investor redemption terms with the underlying asset duration. In these cases, the extension of private credit to retail investors can be viewed as a legitimate expansion of the opportunity set, particularly for income-focused portfolios seeking diversification away from traditional fixed income.

On the other end, there is a growing concern that some offerings are less about democratization and more about distribution. As private credit portfolios mature and underlying borrowers face pressure from higher interest costs, the true economic value of these loans becomes more difficult to ascertain. Unlike public bonds, which are continuously priced by the market, private credit relies on internal models and third-party valuation agents. This creates an environment where marks may lag reality, particularly during periods of credit deterioration.

Growing Private Credit Retail Vehicles

Retail-focused vehicles can, in some instances, serve as an outlet for legacy positions that may be difficult to exit at par in institutional secondary markets. By introducing periodic liquidity windows rather than daily liquidity, managers gain flexibility in managing redemptions, but this also shifts liquidity risk to the end investor. In stressed environments, redemption gates, suspensions, or extended settlement periods become real possibilities—features that retail investors may not fully appreciate when allocating capital.

Additionally, as competition intensifies, underwriting standards may compress. The influx of capital into private credit has already led to tighter spreads and more borrower-friendly terms. If this trend continues, future vintages may not offer the same risk-adjusted returns that defined the asset class over the past decade. Retail investors entering at this stage of the cycle are effectively buying into a more competitive, and potentially more fragile, credit environment.

Looking forward, the trajectory of private credit will likely hinge on how well managers balance growth with discipline. The most durable platforms will be those that maintain underwriting rigor, provide transparent reporting on portfolio health, and clearly communicate liquidity constraints to investors. Meanwhile, investors will need to develop a more institutional mindset, evaluating not just yield, but structure, seniority, and alignment of incentives.

The expansion of private credit into retail portfolios is not inherently problematic. In many ways, it represents a natural evolution of capital markets. But as access broadens, so too must scrutiny. The distinction between accessing yield and inheriting risk will define outcomes in this next chapter of private credit investing.

Disclaimer: I have direct investments in alternative asset managers who manage private credit funds and own private credit assets myself. This post is not a recommendation to buy, sell, or trade any asset or instrument. Please visit my personal portfolio to see my financial positions for clarity of my biases or inclinations. I previously wrote about the private credit market as it was growing, I hope investors understand the risks before engaging in the space.