Modern portfolio construction often assumes that owning both stocks and bonds creates sufficient diversification. For decades, the traditional 60/40 portfolio relied on a simple assumption: when equities decline, bonds rise. That relationship helped investors reduce volatility and stabilize portfolio returns. However, over the past several years, stocks and bonds have increasingly moved in sync, weakening one of the foundational assumptions of traditional diversification. This shift highlights the growing importance of owning uncorrelated assets in your portfolio.

Assets that behave independently from one another provide diversification not simply through asset variety, but through distinct return drivers. When properly integrated, uncorrelated assets can significantly improve portfolio stability and risk-adjusted returns.

Understanding Uncorrelated Assets

Uncorrelated assets are investments whose returns show little or no statistical relationship with traditional equity markets. In portfolio theory, this relationship is typically measured using correlation coefficients and beta.

Correlation measures how closely two assets move together. It ranges from -1 to +1:

- +1 means assets move perfectly together

- 0 means no relationship between returns

- -1 means assets move in opposite directions

Beta measures an asset’s sensitivity to movements in a benchmark, usually the S&P 500. A beta of:

- 1.0 indicates the asset moves in line with the market

- 0.0 indicates no market sensitivity

- Negative beta indicates the asset moves opposite to equities

Assets with low or negative beta often provide the most effective diversification benefits.

The Changing Relationship Between Stocks and Bonds

For much of the past two decades, stocks and bonds exhibited a negative correlation. This allowed investors to combine the two asset classes and achieve smoother portfolio returns.

That relationship has weakened considerably in recent years.

Historical Stock-Bond Correlation

Correlation measured between the S&P 500 Total Return Index and the Bloomberg U.S. Aggregate Bond Index.

| Period | Stock-Bond Correlation |

|---|---|

| 1970–1999 | +0.28 |

| 2000–2010 | -0.35 |

| 2010–2019 | -0.23 |

| 2020–2023 | +0.31 |

| 2022 | +0.61 |

| 2024–2025 (rolling average) | +0.19 |

During the 2000–2019 period, stocks and bonds frequently moved in opposite directions, providing strong diversification benefits. However, inflation shocks beginning in 2020 changed that dynamic.

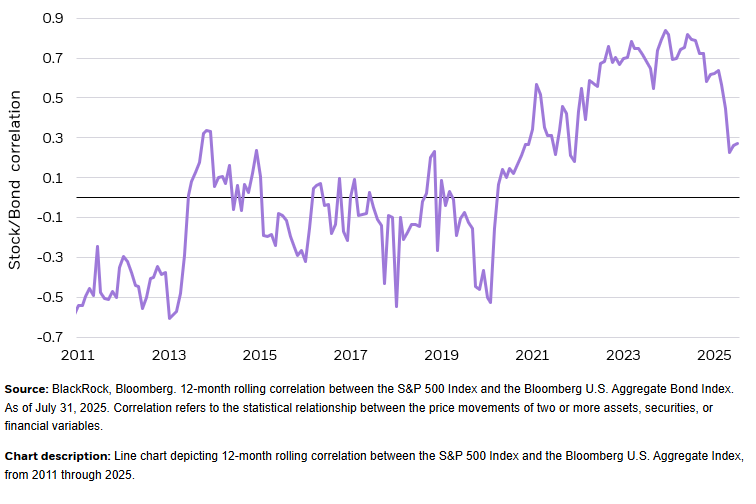

What many allocators still miss is that the stock-bond relationship is regime dependent. BlackRock’s research notes that the post-pandemic environment of higher inflation and rate volatility pushed stock-bond correlation positive, a stark break from the prior two decades, and that this inverse relationship began changing in 2021. Its 12-month rolling correlation work, using the S&P 500 and Bloomberg U.S. Aggregate Bond Index, shows that positive stock-bond correlation remained persistent through July 31, 2025.

When Stocks and Bonds Decline Together

The breakdown in stock-bond diversification became especially evident during the inflation-driven market correction of 2022.

| Year | S&P 500 Return | U.S. Aggregate Bond Return |

|---|---|---|

| 2008 | -37.0% | +5.2% |

| 2013 | +32.4% | -2.0% |

| 2018 | -4.4% | +0.0% |

| 2020 | +18.4% | +7.5% |

| 2022 | -18.1% | -13.0% |

The simultaneous drawdown in both stocks and bonds during 2022 represented one of the largest declines for the traditional balanced portfolio in modern history. The below chart is from BlackRock’s research mentioned above.

When both asset classes decline together, investors relying solely on stock and bond diversification are exposed to significantly higher portfolio risk.

Why Uncorrelated Assets Improve Portfolio Construction

Modern portfolio theory shows that diversification benefits depend primarily on correlation between assets, not simply the number of investments. When correlations rise between core asset classes, portfolios require additional sources of return that behave independently from equity markets.

This is where uncorrelated assets play a crucial role. By introducing assets with different economic drivers, portfolios can reduce volatility and improve risk-adjusted returns even when traditional markets become synchronized.

Beta of Major Asset Classes Relative to the S&P 500

Beta helps quantify how sensitive different asset classes are to equity market movements.

| Asset Class | Representative Index or ETF | Beta vs S&P 500 |

|---|---|---|

| U.S. Large Cap Equity | S&P 500 | 1.00 |

| Investment Grade Bonds | Bloomberg U.S. Aggregate | 0.20 |

| Gold | GLD ETF | 0.19 |

| Commodities | Bloomberg Commodity Index | 0.08 |

| Managed Futures | DBMF ETF | -0.09 |

| Market Neutral Equity | BTAL ETF | -0.52 |

| Global REITs | FTSE EPRA NAREIT | 0.60 |

| Private Equity | Cambridge PE Index | 0.80 |

| Treasury Inflation Protected Securities | TIPS Index | 0.12 |

Several important insights emerge from this data.

Assets such as managed futures, catastrophe bonds, and gold exhibit very low beta relative to the equity market. This means their returns are driven by factors other than corporate earnings or equity valuation cycles.

Conversely, asset classes often perceived as diversified, such as private equity or real estate, can exhibit high equity beta, making them more correlated to stock markets than many investors realize.

Interested in optimizing your portfolio beta? Check out the Portfolio Beta Optimizer to see where you can tweak your positions to meet your goals.

Examples of Uncorrelated Assets

Several asset classes have historically demonstrated low correlation with equities.

Gold

Gold has long served as a monetary asset and inflation hedge. Its price is influenced by real interest rates, currency fluctuations, and global monetary conditions rather than corporate earnings.

Managed Futures

Managed futures strategies trade global futures markets across commodities, currencies, interest rates, and equities. Because these strategies can take both long and short positions, they often perform well during strong market trends, including market crises.

Market Neutral Strategies

Market-neutral equity strategies aim to eliminate broad market exposure by balancing long and short positions. This structure allows returns to be driven by relative value opportunities rather than market direction.

Why Modern Portfolios Need Uncorrelated Assets

Relying solely on stocks and bonds assumes that historical correlations will remain stable. The past several years demonstrate that this assumption does not always hold. When inflation rises or interest rates move sharply, both equities and bonds can respond negatively to the same macroeconomic forces.

In these environments, portfolios that incorporate uncorrelated assets can maintain greater stability because their return drivers differ from traditional markets. The goal is not simply to own more assets, but to own assets that behave differently.

The Bottom Line

Diversification is not defined by the number of assets in a portfolio. It is defined by how those assets interact with one another.

As correlations between stocks and bonds fluctuate across economic regimes, investors increasingly need uncorrelated assets to maintain effective diversification. Assets such as gold, managed futures, and market-neutral strategies provide return streams that are driven by different economic forces than equities and traditional fixed income.

In modern markets, incorporating uncorrelated assets is no longer optional for investors seeking true diversification, it is an essential component of robust portfolio construction.